Is $TRU a productive asset?

Is $TRU a productive asset?

Yes, yes it is.

Going off the last post, where we broke down the difference between ‘weak productive assets’ and ‘strong productive assets’, in this post we will ask if TrueFi’s $TRU token is or is not a strong productive asset?

In our last post we defined ‘strong productive assets’ as assets that are core to the functioning of and/or core economic activity of the protocol. Strong productive assets are directly entitled to a protocol’s cash flows either through direct payments or deflationary mechanisms such as token burns.

What is $TRU and how is it used?

$TRU is TrueFi’s protocol token used for governance and staking.

From the TrueFi blog:

TRU is today used for

Staking on TrueFi, which allows for new loans to be approved or rejected, and also provides some protection to TUSD lenders in case of loan default. Stakers are rewarded in TRU & tfTUSD for their participation.

TrueFi governance, which demands TRU (or stkTRU) for on-chain votes to enact protocol-level changes, as well as allowing TrueFi community actions such as providing grants from the TRU community treasury.

Providing liquidity on DEXs like Uniswap or Sushiswap. Liquidity Providers (LPs) are typically rewarded with a share of the transaction fees collected on the pair they’re supporting, and may sometimes enjoy farming incentives. View TrueFi’s current farms here.

Per TrueFi’s documentation:

“Staking TRU on the protocol enables Stakers to earn a portion of the loan origination fees generated by the TrueFi protocol. Currently, Stakers earn 100% of the fees generated by the TrueFi protocol.

The loan origination fees generated by TrueFi will be lent to the TrueFi TUSD Pool in exchange for tfUSDC tokens and stakers will be rewarded with the tfUSDC tokens. The proportion of fees paid to stakers can be changed through protocol governance.”

At launch, TrueFi charged borrowers a 0.25% origination fee for each new loan generated on the platform. 100% of those fees went to protocol stakers, paid in the form of tfTUSD.

As of late May, the origination fees were eliminated in exchange for stakers receiving a 10% cut of interest generated. This is paid to stakers in the form of tfUSDC, a yield bearing deposit token.

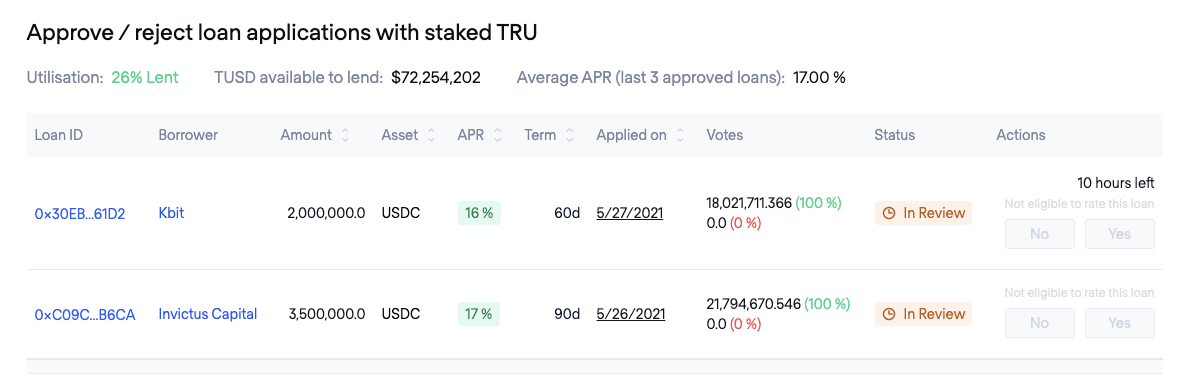

The individuals staking on the protocol are also providing a partial backstop to lenders in the case of a default. As I am writing this, 102,581,728 TRU ($33,851,970.24) are staked on the platform. In the event of a default, borrowers could have up to 10% of their staked TRU slashed in order to make lenders whole on their loss.

The individuals who are staking their TRU are also eligible to ‘rate’ individual loan requests. You can see below that Invictus Capital and Kbit both had unanimous support for their loan requests. This in part because these are both repeat borrowers. This gives stakers an additional layer of power in deciding who is able to borrow from TrueFi.

Is TRU a Strong Productive Asset?

Breaking our definition into two parts:

Assets that are core to the functioning of and/or core economic activity of the protocol.

YES. Loans cannot be approved without stakers rating individual loan requests. Stakers also provide a backstop to defaulted loans. Arguably, this is a core function of the protocol because without it, it might be hard to attract lenders.

Assets that are directly entitled to a protocol’s cash flows either through direct payments or deflationary mechanisms such as token burns.

YES. Since day 1, stakers have been partially entitled to protocol fees, but in the latest V3 upgrade, this is even clearer with stakers receiving 10% of the interest generated by repaid loans.

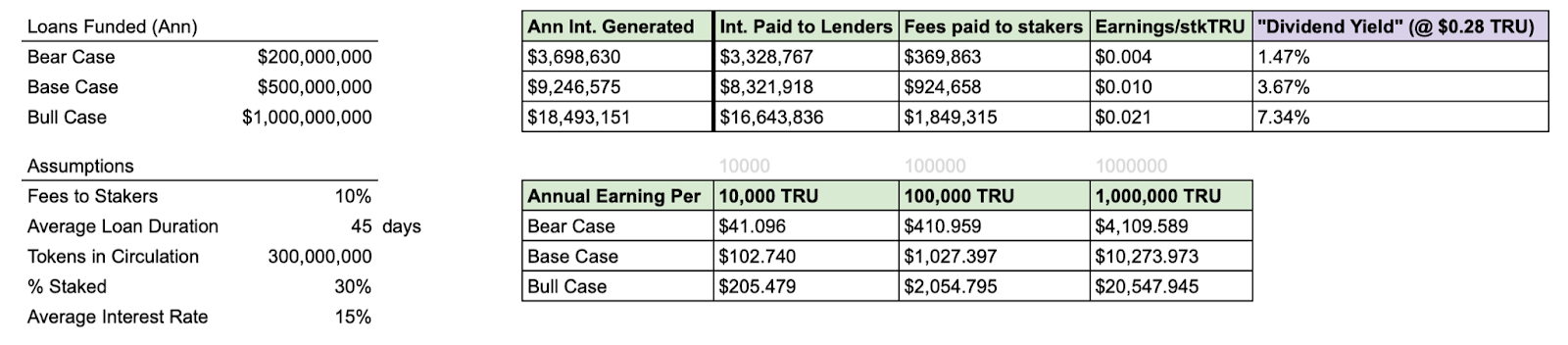

How Good are TrueFi’s Cash flows?

The short answer is that they’re OK for a 6-month old protocol.

Projecting forward though, it’s easy to see how these can quickly get juicy.

(Source -- Please make a copy if you want to play around with the #’s)

Like a lot of protocols that are still bootstrapping, TrueFi has a ‘yield farming’ component. We covered above how TRU stakers earn protocol fees, but we didn’t mention that they also earn a TRU denominated yield of about 30-50%.

These staking rewards are designed to run for about 3-years and they act as a way to incentive staking while protocol fees are still relatively low. At the end of that 3-year period (hopefully earlier), TrueFi will be originating loans in the billions per year and the $$-denominated fees paid to stakers will be in the double-digit range, rendering $TRU incentives less meaningful.

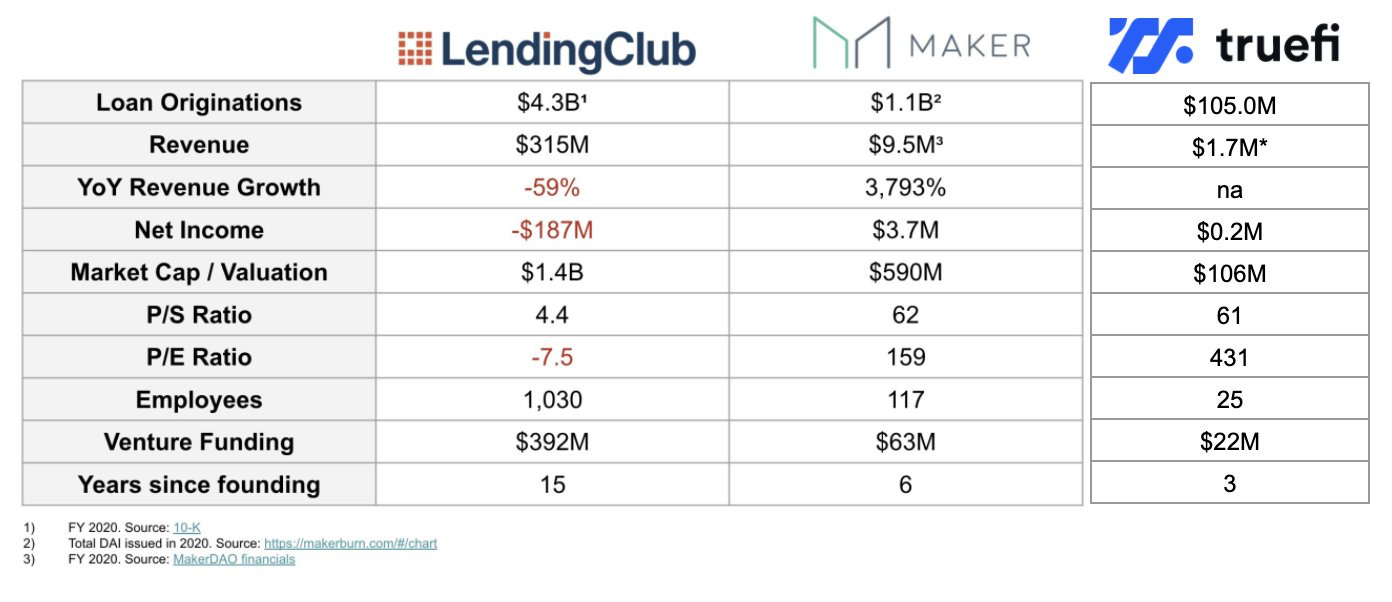

As @TylerWallace pointed out in a recent Twitter thread, TrueFi is in its very early days, but you can see how this can get big.

(Source: Tyler Wallace’s Twitter)

The big difference as Tyler points out between DeFi and TradFi is that TradFi lending companies often take years to generate positive cash flow, whereas DeFi can get there in months.

Looking at the kind of origination volumes and revenues that the large crypto lenders (Genesis and BlockFi) do, TrueFi getting to 1bn in originations in its first year without completely overextending its risk profile seems very reasonable.

Thank you to @RyanRodenbaugh and @wtylerwallace who contributed greatly to this post.